The world's largest asset class has spent decades sitting outside capital markets. Not because it lacked value. Not because investors were not interested. But because it lacked the one thing institutional capital cannot move without: regulated financial structure.

That changes today.

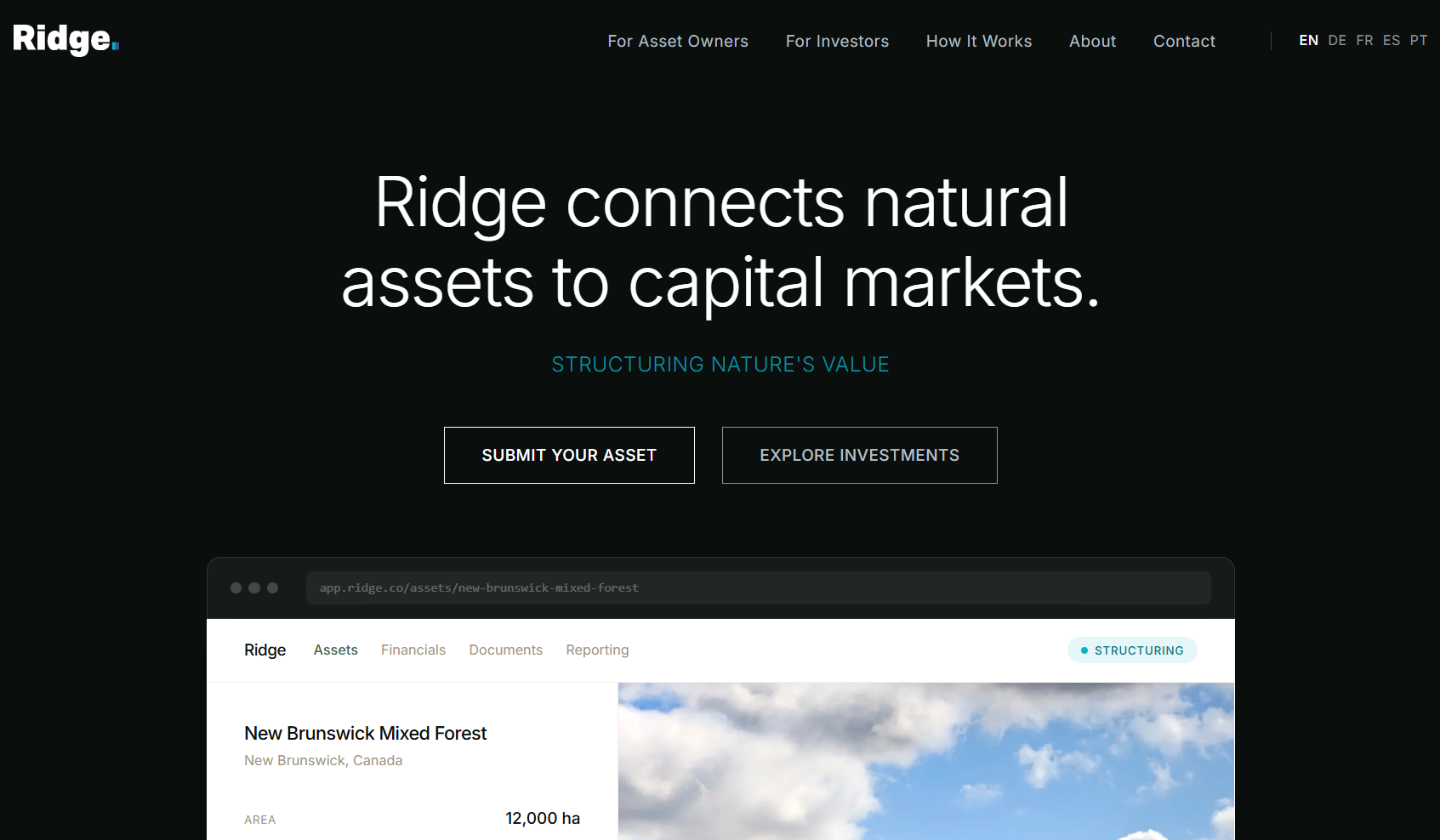

Ridge has launched the financial infrastructure that converts natural assets - forests, regenerative agriculture, conservation-linked land - into regulated, ISIN-listed, investment-grade securities. A sustainably managed forest in Canada or a regenerative rubber plantation in Guatemala can now be held, reported on, and traded through the same financial infrastructure institutions already use for bonds, private credit, and real estate.

The Structural Gap

Natural commodity production represents a total available market of $9-10 trillion. It offers long-duration, inflation-linked returns with historically low correlation to equities, bonds, and real estate - precisely the characteristics institutional allocators are actively seeking in today's market environment.

The demand is not in question.

- 79% of institutional investors show active interest in natural assets

- 90%+ of pension funds and insurers plan to invest or increase allocation by 2030

- Timberland funds raised nearly 3x more capital in 2024 than in 2019

- The global impact investing market already exceeds $2.5 trillion

Yet despite surging allocation intent, the vast majority of this capital remains on the sidelines. The reason is not conviction. It is infrastructure.

Natural assets, as they exist today, lack standardised structuring, regulatory compliance, ISIN issuance, performance reporting, and secondary market liquidity. The existing alternatives - voluntary carbon credit schemes, unregulated marketplaces, illiquid timberland funds - do not clear the compliance, custody, or due diligence bar that institutional capital requires. Roughly $225 billion in sustainably managed natural assets sits outside capital markets entirely. U.S. farmland alone is a $3.4 trillion asset class with less than 2.5% institutionally owned.

Ridge does not need to create demand. It needs to remove the friction that is holding committed capital back.

The gap is not appetite. The gap is infrastructure.

Why Now: Four Forces Converging

Ridge does not enter this market on a thesis. It enters at a precise moment when four structural forces converge to make natural asset infrastructure not just viable - but inevitable.

Regulatory Acceleration

EU Taxonomy, SFDR, and net-zero mandates are forcing institutional capital toward sustainability-aligned instruments. But the market lacks regulated supply. Ridge fills that gap with compliant, verified products built specifically for this regulatory environment.

Institutional Rotation

Post-2022, allocators are moving toward real assets and uncorrelated returns as traditional portfolios underperform. Natural assets offer exactly that: long-duration, inflation-linked exposure with genuine diversification value.

Infrastructure Maturity

Securitisation frameworks, digital issuance infrastructure, and the emergence of tokenisation - projected to reach $16 trillion by 2030 - have dramatically lowered the cost and complexity of structuring natural assets into tradeable securities.

ESG Fatigue

Institutional capital is moving away from narrative-driven ESG toward regulated, verifiable, asset-backed instruments. Ridge is built precisely for this shift - financial plumbing first, impact embedded in the structure, not painted over it.

What Ridge Has Built

Ridge closes the infrastructure gap. The platform delivers the complete stack required to convert natural assets into regulated financial products: origination, validation, structuring, distribution, and ongoing monitoring - integrated end to end.

Each natural asset undergoes in-depth due diligence, including on-site verification and independent valuation, before being structured into an ISIN-eligible security.They are distributed through existing banking and brokerage infrastructure - held in standard custody, clearing, and settlement systems. No operational change is required from the investor.

This is not a concept. Ridge has already done it.

Proof Points - Operational, Not Aspirational

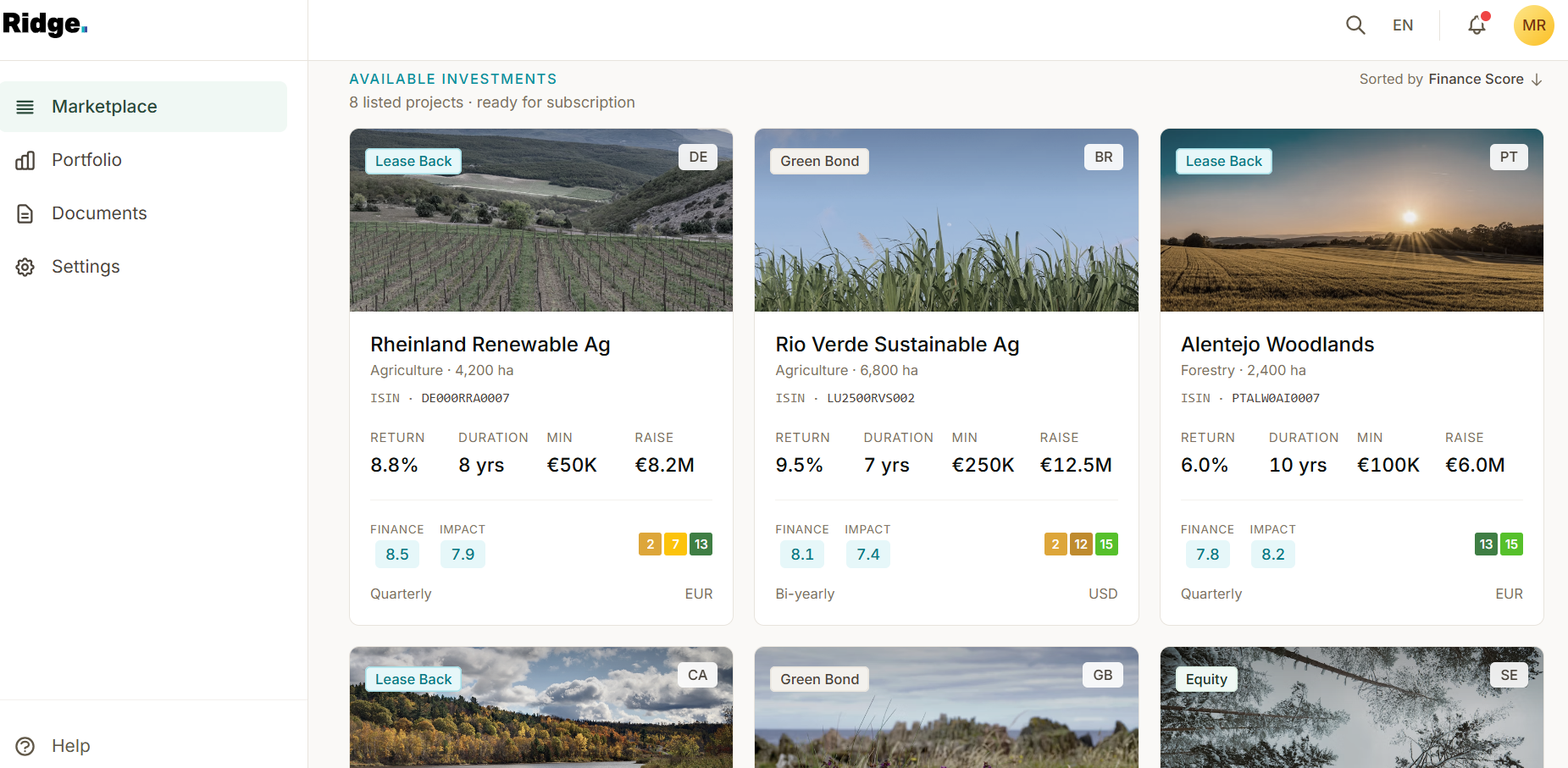

- 4 regulated financial products issued with ISIN numbers under BaFin framework

- Partnerships with 3 German banks and 2 alternative asset platforms

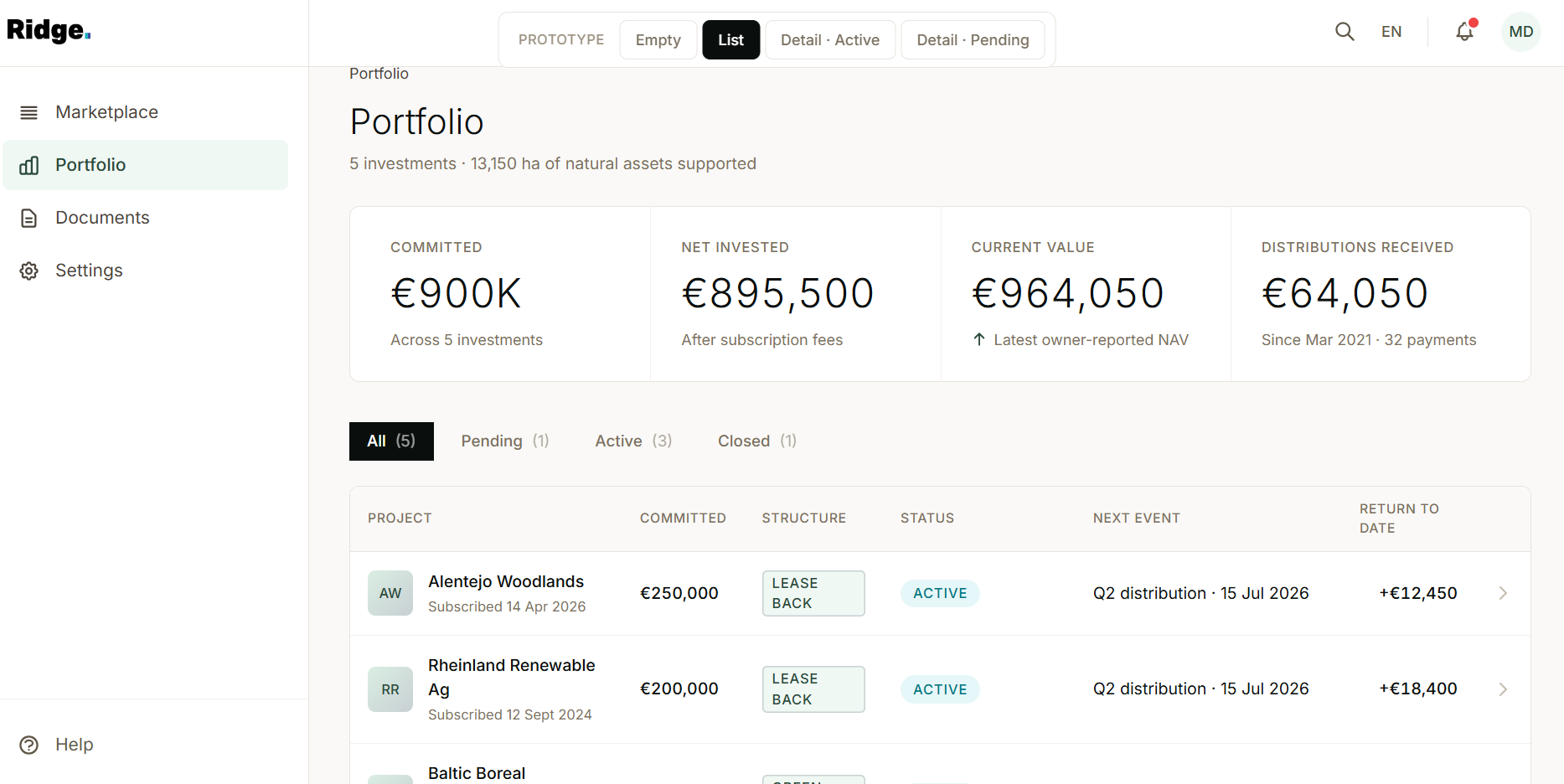

- €100M+ active pipeline in global natural asset projects

- IRR profiles between 5-12% across pipeline assets

- Investments secured from Family Offices and HNWI

Others sell access or stories. Ridge builds markets.

The Missing Piece - Not Another Fund

The market already has impact funds, green bond issuers, timber private equity, and niche fractional platforms. None of them solved the structural problem.

Impact funds pool capital but issue no regulated securities, no ISINs, no secondary market. Green bonds fund corporate balance sheets, not direct exposure to verified natural assets. Timber and farmland private equity structures are illiquid, high-minimum, and non-standardised. Niche platforms are unregulated, jurisdiction-limited, and carry no institutional credibility.

Ridge does not compete inside any of these categories. Ridge owns the admission layer - the regulated infrastructure that sits above all of them. From natural asset to ISIN to institutional investor, Ridge controls the full stack. Once institutional capital expects natural assets to be structured and regulated, everything outside Ridge's framework becomes uninvestable by default.

What is regulated gets trusted. What is structured gets allocated. What is listed gets defended.

Built to Last: The Moat

First-mover advantage in a regulated asset class compounds differently from any other market. Ridge is the only platform converting commodity-backed natural assets into regulated financial products tradeable by banks and brokers. That position deepens with every product issued, every institutional relationship built, and every data point generated.

Regulatory Moat

Issuing financial products under the BaFin framework is one of the most rigorous financial regulatory processes in Europe. The compliance infrastructure Ridge has built is expensive, slow to replicate, and durable. Regulation is not a hurdle Ridge cleared - it is a barrier Ridge now sits behind.

Data Moat

Every issuance, every verified natural asset, every performance report adds to Ridge's longitudinal dataset across natural asset classes. Over time, that dataset becomes the benchmark for pricing, risk modelling, and allocation decisions in the category. No new entrant can buy their way to that.

Category Moat

Ridge does not compete in an existing marketplace. It defines the admission layer for a new asset class - what qualifies, how it is structured, what standards apply. Owning the category definition is the deepest moat available. When the category matures, Ridge is the infrastructure it runs on.

Expectation Moat

Once institutional investors expect natural assets to arrive structured, regulated, and ISIN-listed, unstructured nature becomes uninvestable by default. Ridge sets the standard. Everything outside it becomes substandard.

The Founder's Perspective

"Nature is not an alternative asset. It is the original one - the substrate the rest of the economy is built on. For decades, institutional capital has been unable to hold it at scale, not because the returns were not there, but because the financial wrapper was not. Ridge has built that wrapper: regulated, ISIN-listed products that integrate with the custody, reporting and mandate frameworks allocators already use. Today we are open for business."

Who Ridge Serves

Institutional Investors - Pension Funds, Insurers, Sovereign Wealth

Regulated, compliant exposure to natural assets as a distinct portfolio allocation. Uncorrelated returns, inflation protection, and instruments that satisfy sustainability mandates and fiduciary standards - through existing custody, banking, and trading infrastructure. No operational change required.

Professional Investors and Asset Managers

A new asset class with genuine diversification value, structured to institutional standards. ISIN-listed products that fit existing portfolio construction and client reporting workflows, with standardised performance data and transparent impact reporting.

Asset Originators - Forest Owners, Agricultural Producers, Regenerative Projects

A credible pathway from unstructured natural asset to regulated financial product. Ridge replaces fragmented, costly, and reputationally risky monetisation options with efficient access to institutional capital through BaFin-regulated instruments.

Backed by Disrupt

Ridge is supported by Disrupt, a MENA-based venture building partner and investor with over 17 years of experience and $1B+ in aggregate value created across its portfolio. Disrupt builds AI-native platforms designed to address structural gaps in global markets - combining venture funding with hands-on operational support. That model enabled Ridge to develop as a fully integrated platform, from regulatory approval through to product issuance and institutional distribution.

The Infrastructure Is Live

Natural assets have always produced value. Land feeds economies. Forests stabilise climates. Regenerative systems generate returns quietly, while capital markets looked elsewhere.

That is no longer the case.

Four regulated products are issued. Three bank partnerships are live. A pipeline exceeding €100 million is under active structuring. BaFin approval is secured. The institutional rails are in place.

And the roadmap goes further. Ridge is building toward secondary market infrastructure from inception - enabling price discovery, liquidity, and long-term market viability. Markets only mature when exit exists. Ridge builds toward tradeable, liquid natural asset securities, making nature not just investable today, but a permanent and defended asset class for the decades ahead.

Ridge is not a concept.

Ridge is operational.

And this is just the beginning.

Explore Ridge's regulated product range or request an investment memorandum at ridge.global

.avif)